The package includes the video recording, the slide deck, and pre-filled templates with worked examples for reporting different solo and group structures.

The webinar took place on 10 June 2026. It was open to the public and drew more than 2,500 participants. The session gave an overview of how AMLA will select obliged entities for direct supervision from 2028, together with a practical walkthrough of the eligibility reporting package. This included live demonstrations of the templates that obliged entities will be required to submit when requested by their national financial supervisor.

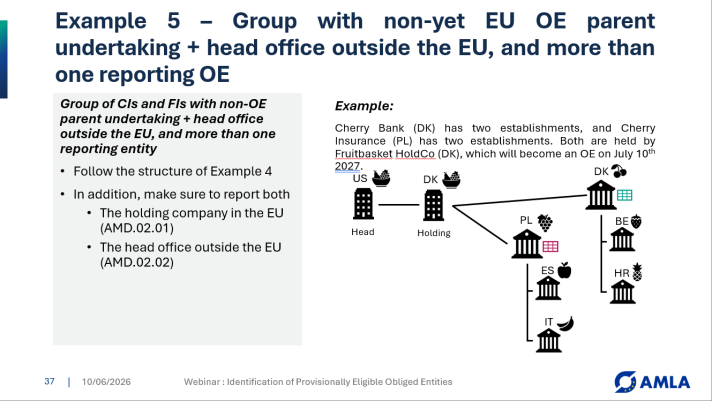

The materials below are intended as practical guidance for all reporting obliged entities.

AMLA values the strong engagement shown by participants and is currently reviewing the many questions received during and after the webinar. A dedicated FAQ document covering the most frequently raised points will be added to this package in the coming days.

Materials

Slide deck

Download

Please note: as mentioned during the session, the slides shown contained typographical errors that have since been corrected. Please refer only to the PDF version provided here.

Examples and pre-filled templates

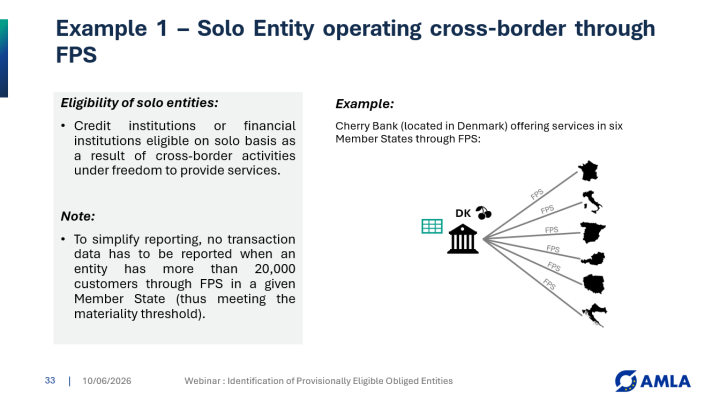

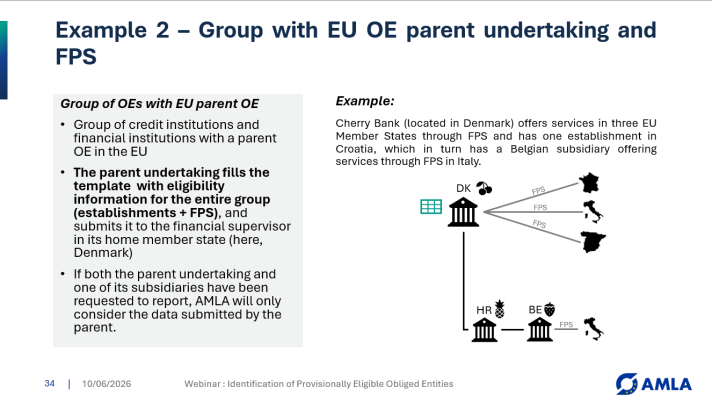

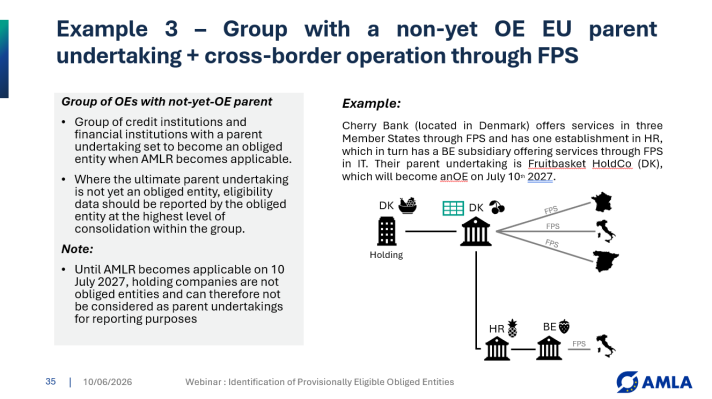

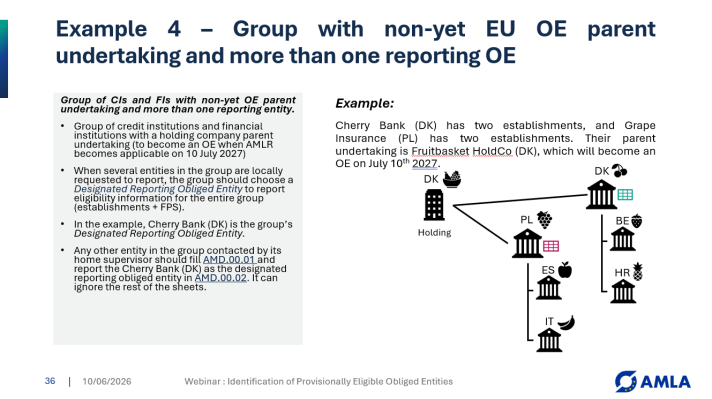

The pre-filled templates below illustrate how to report different solo and group structures. Each example is accompanied by the corresponding slide from the webinar.